#049 Venture Capital Investing Mindset: Understanding India’s Strategic Approach

Thu, 09 Apr 2026 07:10:17 GMT

Cornerstone Ventures

As an Indian venture capitalist, I’ve often been asked why our investment philosophy differs so dramatically from our American counterparts. The answer isn’t simply about being more conservative or less ambitious—it’s about understanding the unique dynamics of our market and building a sustainable model that creates genuine value for founders and investors alike.

The American Power Law: Swing for the Fences

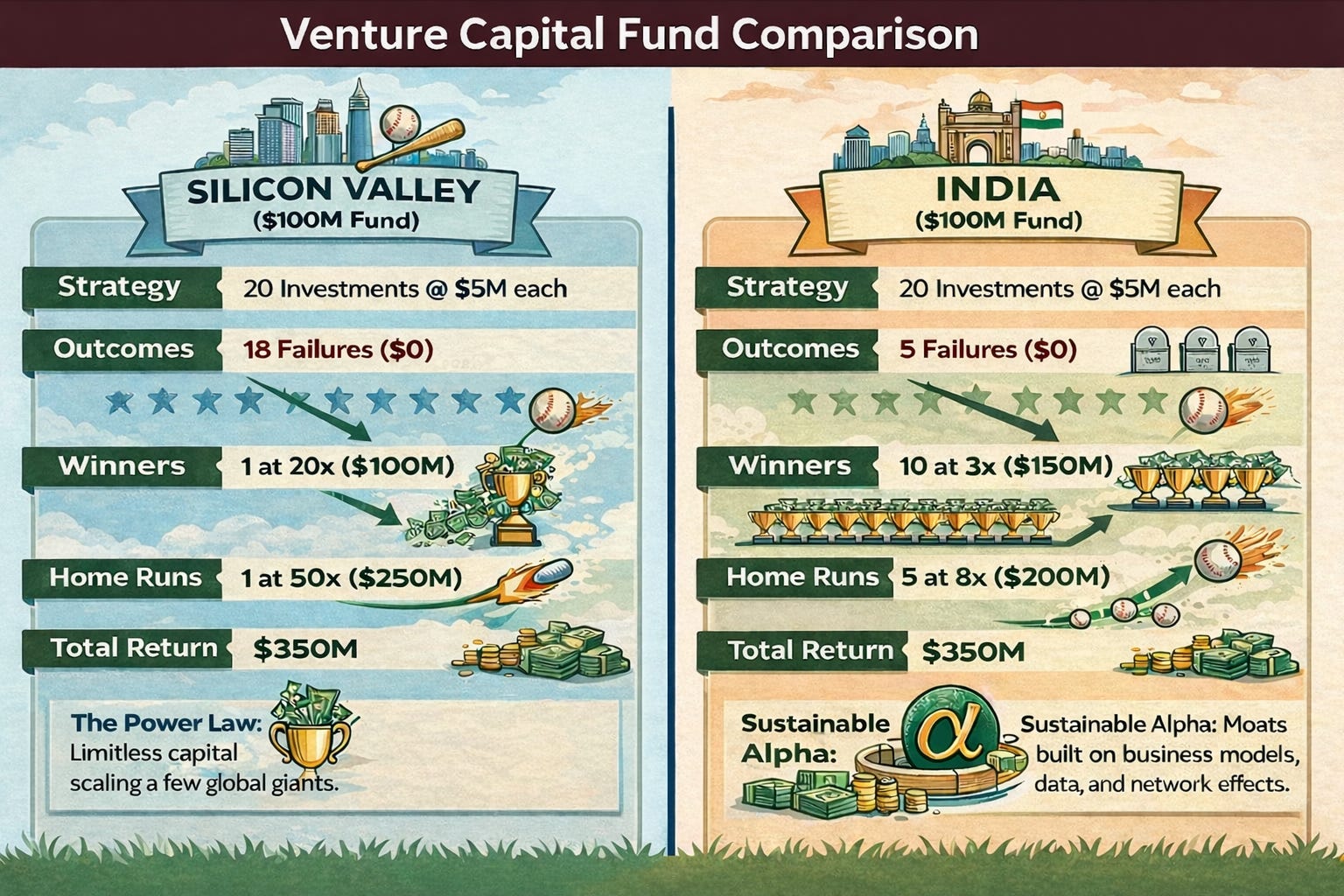

The US venture capital model is elegantly simple in theory: invest in 30-40 companies, expect most to fail, a few to break even, and pray that one becomes the next Uber or Airbnb. This power law approach means that a single investment returning 100x can compensate for all the losses in a portfolio. Sequoia’s investment in WhatsApp, which turned $60 million into $3 billion, or Benchmark’s $12.7 million bet on Uber that became worth over $7 billion—these are the home runs that define American VC success.

This strategy works in an ecosystem with large scale patient capital availability, mature exit mechanisms and evolved risk tolerance. The US offers robust IPO markets where companies can go public at massive valuations, deep M&A activity with tech giants paying billions for strategic acquisitions, and a culture that celebrates moonshots. Failure is not just tolerated—it’s almost a badge of honor, a necessary stepping stone to eventual success.

India’s Reality: Building Sustainable Returns Through Multiple Wins

Our approach in India is fundamentally different, and for good reason. We construct focused portfolios with 15-20 investments, writing smaller initial checks and reserving capital for follow-ons in our winners. Success here isn’t about finding the one unicorn that returns the fund ten times over—it’s about building a portfolio where 10-15 companies deliver solid 3-5x returns, with a handful achieving 10-15x outcomes.

Consider the practical realities we navigate. When Flipkart was acquired by Walmart for $16 billion in 2018, it was celebrated as India’s largest startup exit. Compare this to Uber’s $82 billion IPO—the scale is simply different. Even recent successes like Zomato’s IPO, valued at approximately $8 billion, or PolicyBazaar at $6 billion, while impressive, operate in a different magnitude than their American counterparts.

This isn’t a limitation—it’s our market reality emanating from lack of high risk appetite capital available for VCs and startups. Indian VCs who recognized this early and built portfolios accordingly have delivered exceptional returns. The key is understanding that multiple strong exits create sustainable fund performance, rather than relying on a single outlier to carry the entire portfolio.

Why India’s Model Makes Strategic Sense

Our emphasis on business fundamentals isn’t conservative—it’s essential. In a market where risk capital availability is limited and exit valuations are more grounded, we can’t afford to back companies burning cash indefinitely on the promise of network effects. We look for businesses with clear unit economics, realistic paths to profitability, and defensible competitive advantages.

In 2025 Indian VC invested approximately $11 billion whereas single deals in the US ecosystem were much larger than this. For e.g. OpenAI alone raised $40 billion in 2025.

In fact, some of our largest platforms are even bootstrapped. Take Zerodha, India’s largest stockbroker, which bootstrapped its way to profitability and is now valued at over $3 billion. Or Zoho, which chose sustainable growth over venture funding and built a $1 billion+ SaaS business. These examples reflect a broader truth about the Indian market: sustainable business models often outperform growth-at-all-costs strategies.

The exit environment shapes this thinking. While India’s IPO market has matured significantly—we saw 103 IPOs in 2025 raising $20.5 billion—the valuations and market receptivity remain more measured than in the US. Strategic acquisitions, while growing, rarely reach the billion-dollar marks common in Silicon Valley. This reality demands portfolio construction that doesn’t depend on outlier outcomes.

While India’s tech landscape has matured rapidly, Silicon Valley maintains a distinct set of structural advantages:

Network Density: Unmatched concentration of capital, innovation, and a self-sustaining ecosystem.

Global GTM Dominance: A “default-global” brand and established market-access playbooks.

Cultural Edge: A deep-tech bias paired with a radical appetite for risk and rapid iteration.

Conversely, Indian counterparts still navigate specific structural constraints:

Ecosystem Gaps: Despite progress, India still faces hurdles in foundational R&D, advanced semiconductor nodes, and the sheer scale of product ecosystems found in the US.

Infrastructure & Brand: Regulatory frameworks and global brand recognition for “Made in India” SaaS and deep-tech are still in an evolutionary phase.

Access to Scale: Time zones, local market nuances, and the depth of late-stage, high-risk funding still lean heavily in favor of the West.

The Venture Math: Two Paths to the Same Return

Despite these constraints, Indian VCs have mastered a different path to liquidity. While Silicon Valley relies on the Power Law (where a single outlier pays for the entire fund), the Indian model often relies on higher hit rates and capital efficiency.

Here is how two $100M funds might arrive at the same $350M outcome using vastly different strategies:

Our Competitive Advantage

Understanding these differences isn’t about aspiring to replicate the American model—it’s about recognizing our strengths. Indian VCs bring thoughtful capital, operational support, and realistic expectations that align well with founders building sustainable businesses. We understand local market dynamics, regulatory complexities, and the importance of capital efficiency in a market where funding winters can be harsh and prolonged.

As India’s startup ecosystem matures, we’re seeing the best of both worlds emerge: founders with global ambitions building businesses grounded in strong fundamentals, and VCs who can support moonshots while maintaining portfolio discipline. That’s not compromise—that’s strategic sophistication.

~ Abhishek

Learn more about: Cornerstone Ventures | CGES Index

Disclaimer:

The data provided on this website (www.csvpfund.com) is for informational purpose only.

Any information provided on this website or any of the other digital assets owned & maintained by Cornerstone Venture Partners Fund, Mumbai, India (“CSVP”)and managed by the Investment Manager, Cornerstone Ventures Investment Advisers LLP, Mumbai India, does not constitute investment advice or investment recommendation nor does it constitute an offer to buy or sell or a solicitation of an offer to buy or sell shares or units in any of the investment funds or other financial instruments.

The Cornerstone Global Enterprise SaaS Index (“CGES Index”) ™ is a trademark of CSVP. The CGES Index is created & maintained using a proprietary algorithm and is to be used for informational purpose only. It is not to be construed as an investment advice or investment recommendation in any of the constituent companies / stocks that are directly or indirectly part of the Index. The Index is created using publicly available data published on the websites of the respective companies. All data presented is as per our internal research and analysis leveraging publicly available data and is being presented only for academic deliberation and discussion purposes and is not to be viewed as any specific commentary / recommendation / evaluation / conclusion on any of the companies / stocks that are directly or indirectly part of the CGES Index.

CSVP also analyses, maintains, and publishes certain financial and non-financial metrics (“SaaS Metrics”) on the Index at an aggregate level, and not at a specific company / stock level that constitute the CGES Index. These SaaS Metrics are provided purely for informational purpose and CSVP assumes no liability for accuracy, suitability, or completeness of the SaaS Metrics. The SaaS Metrics are created using publicly available third-party information and CSVP does not claim any ownership of the sourced data. CSVP is not responsible for the accuracy, suitability or completeness of the information originally disclosed by the owner of the information and any information provided herein. CSVP accepts no liability and offer no guarantee as to whether the information is up to date, correct or complete.

CSVP may have used third-party data, information, and content (including all text, data, graphics, and logos) on the website. CSVP assumes no ownership and intends no infringement of rights, titles, and claims (including copyright, brands, patents and other intellectual property or other rights) of the respective owners or authorized users of the respective content. Use of such content is from publicly available sources and for indicative and informational purpose only in good faith. All trademarks and registered trademarks are the properties of their respective owners. This website may contain references or links to other websites. References and links to third-party websites do not mean that CSVP adopts the content behind the reference or link as its own. When first setting up the link, CSVP will have checked the linked site for illicit content and found none at that time. However, CSVP have no influence over the current and future design or content of such linked sites and will accept no liability for such content or design. Any use of these websites is at your own risk. The obligation of CSVP to remove or block the use of information according to the general laws from the time of knowledge of a concrete violation of the law remains unaffected.

X

Contact Us

contact@csvpfund.comGet our latest updates on

.svg)

.svg)

Contact Us

contact@csvpfund.comGet our latest updates on

Contact Us

contact@cornerstoneventures.vcGet the latest updates on

Cornerstone Venture Partners Fund

9 Aug 2018

IN/AIF1/18-19/0572

Cornerstone Ventures Investment Fund

11 Dec 2023

IN/AIF2/23-24/1406

Contact Us

contact@csvpfund.comGet the latest updates on

Cornerstone Venture Partners Fund

9 Aug 2018

IN/AIF1/18-19/0572

Cornerstone Ventures Investment Fund

11 Dec 2023

IN/AIF2/23-24/1406

Copyright © 2025 Cornerstone.

All Rights Reserved.